If you’ve ever signed up for Stripe, Square, or PayPal and started accepting credit card payments almost instantly, then you’ve already experienced what it’s like to use a payment facilitator, also known as a PayFac.

For many business owners, it seems like a dream: quick setup, no red tape, and everything bundled into a clean platform. And in the early stages of a business, that kind of simplicity is hard to beat.

But what most entrepreneurs don’t realize is that the very thing that makes PayFacs so convenient can also make them risky, especially as your business grows.

In this post, we’ll break down:

- What a payment facilitator actually is

- The real pros and cons

- And when it’s time to switch to a solution built for scale like Easy Pay Direct

Let’s dive in.

Table of Contents

What Is a Payment Facilitator?

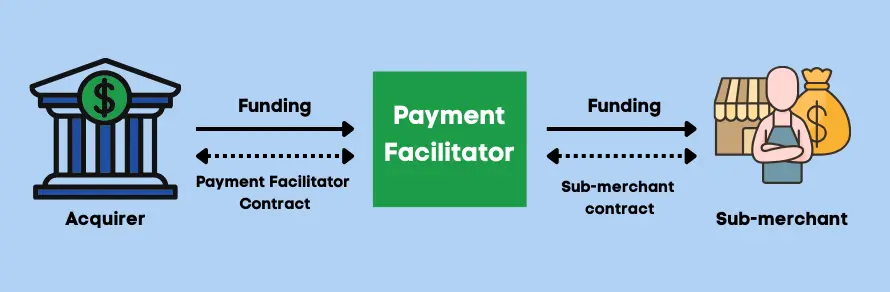

A payment facilitator is a company that allows you to accept credit card payments by operating under its own master merchant account. You’re onboarded quickly, often instantly, as a sub-merchant under the facilitator’s umbrella.

It’s kind of like subletting an apartment. You don’t hold the lease; you’re just living under the name of the main leaseholder. That setup gets you in the door fast, but there’s a downside.

What’s missing in this process is underwriting, the vetting that traditional processors use to understand your business model, products, history, and risk level. Skipping that step makes your account more vulnerable to freezes, held funds, or shutdowns.

We’ll explore these risks in more detail below.

Beware the ‘Set Up in Minutes’ Promise. It Could Cost Your Business

There’s no denying it. Signing up with a payment facilitator is fast. In just minutes, you can be set up and ready to accept payments with almost no effort.

But that speed is exactly the problem. What looks like “instant” convenience often hides serious risks: zero control, sudden account freezes, withheld funds, and little to no support when things go wrong. The very thing that makes PayFacs attractive at the start is what makes them dangerous as your business grows.

Worse, many entrepreneurs don’t even realize they’re relying on Stripe or another PayFac. Platforms like Shopify and HubSpot quietly run on Stripe in the background. So even if you think you’re choosing a supportive platform partner, you’re still locked into Stripe’s rules, risks, and restrictions.

This is the reality countless merchants face, and it proves that “fast and easy” in payments can end up being one of the costliest mistakes your business makes

The Hidden Risks Behind PayPacs

The speed and simplicity of PayFacs exist because they skip traditional underwriting. But that shortcut comes at a cost.

The Hidden Cost of Skipping Underwriting

As a consumer, you can dispute a credit card charge up to six months after the transaction, and if the business has closed, the processor is responsible for the refund. That means every PayFac is constantly weighing the risk of a business closing, the likelihood of chargebacks, and the volume of transactions being processed.

Without underwriting, however, PayFacs have no real visibility into who you are, what you sell, or how you deliver. To protect themselves, their only option is reactive: freeze accounts, hold funds, or shut down merchants altogether.

What can trigger that? Often very little. A sudden spike in sales, a single large transaction, or simply operating in a category they deem “high-risk” can be enough to put your money on hold overnight.

Even worse, because all merchants operate under the PayFac’s master account, the risk is pooled. If a competitor in your industry triggers red flags, the entire category may be flagged, meaning your account could be shut down through no fault of your own.

The consequences can be devastating. What would happen if you couldn’t access your revenue or accept payments for 90 days? For most businesses, payroll, inventory, and growth would grind to a halt. Stretch that to six months, and survival itself may be in question.

We recently saw a real-world example of this when a small, family-owned service business had their account shut down by a PayFac days after onboarding, with funds held despite completed work and authorized payments, highlighting how little control merchants actually have under this model. Read the full story here.

Customer Service That’s Non-Existent

Another major drawback is their customer service. Instead of direct support, merchants are funneled into phone trees and generic queues, where rigid policies often replace real solutions.

Many report that service feels virtually nonexistent, issues can arise without warning, and there’s no dedicated contact to help resolve them.

Flat-Rate Pricing That Gets Expensive Fast

Then there’s the cost. Most PayFacs rely on flat-rate pricing (e.g., 2.9% + 30¢ per transaction). While that structure seems simple at the start, the fees compound quickly as your volume grows. And without a direct relationship with the acquiring banks, you have no ability to negotiate better rates, leaving you locked into pricing that becomes increasingly expensive over time.

Here is a rate comparison chart with a client who came to Easy Pay Direct from Stripe. Although Stripe claimed they were paying 2.9% + 30¢, their effective rate was actually 4.54%, costing them over $75,000 in extra fees:

How Easy Pay Direct Is Different

Unlike PayFacs, Easy Pay Direct doesn’t lump your business under a shared account. We provide true merchant accounts, built specifically for your business and backed by direct banking relationships. We thoroughly underwrite your account from the start, which means you can worry less about shutdowns and unexpected freezes.

Instead, you get real long-term stability, supported by a dedicated team that not only solves issues if they arise but helps optimize your payments strategy for the lifetime of your account.

Why Businesses Choose Easy Pay Direct

✅ Dedicated Support Team

You get a single point of contact who understands your business and works with you to optimize and protect your account over the long term.

✅ Smart Gateway Technology

We built a gateway that allows you to put multiple merchant accounts into it and automatically distribute volume across them. If one of your accounts gets shut down or has an issue, the others are still up and running.

✅ High-Volume & High-Risk Friendly

Whether you’re processing $50K a month or scaling into the millions, Easy Pay Direct is built to handle complex, high-volume, and even “hard-to-place” industries. With access to 30+ back-end banking relationships, we can approve nearly every vertical, including those often labeled as high-risk.

✅ Custom Pricing at Scale

Flat-rate PayFac fees eat away at margins. With Easy Pay Direct, pricing is tailored to your volume and risk profile, helping you save significantly as you grow.

When a Payment Facilitator Makes Sense

If you’re just getting started, testing an idea, selling a few products, or launching a side hustle, a payment facilitator can be a good option.

It’s fast, easy, and requires almost no paperwork. You can start accepting payments within minutes, without the hassle of underwriting or approvals.

This setup works well for:

- Low-volume businesses under $10,000 per month

- Low-risk physical products

- Early-stage entrepreneurs getting the business off the ground

In those early days, the convenience often outweighs the downsides.

But once your volume grows, or if you’re in a more complex industry, those same PayFacs can quickly become a liability. That’s when it’s time to look at more stable, scalable solutions like Easy Pay Direct.

Moving Beyond the Payment Facilitator: The Next Step for Scaling

Payment facilitators are a convenient starting point. But if you’re serious about scaling, and you want long-term stability, predictable cash flow, and real support, it’s time to move beyond the PayFac model.

That’s why thousands of entrepreneurs choose Easy Pay Direct. Because they’re not just looking to process payments; they’re building businesses that can scale with confidence.

👉 Ready to do the same? Get started with Easy Pay Direct today.